Why Are Homeowners Insurance Rates Rising So Fast?

For many homeowners, the first big clue that insurance costs are rising isn’t when they buy the policy — it’s when the renewal notice shows up. The house hasn’t changed. The mortgage payment hasn’t changed. But the insurance premium has gone up, sometimes by a lot.

That change can feel frustrating, but it’s becoming more common. Homeowners insurance has always been part of the cost of owning a home, but today it’s taking up a bigger share of the monthly budget than many people expect.

What Home Insurance Actually Does 🛡️

At its core, home insurance protects against major losses like fire, storms, theft, and other expensive surprises. Instead of taking on that risk alone, homeowners pay a premium so those costs are more manageable if disaster strikes.

Insurance also plays a second important role: most lenders require it. Since the home is the lender’s collateral, insurance helps protect both the homeowner and the mortgage system if something goes wrong. That’s why it’s not just a nice extra — it’s a required part of most home purchases.

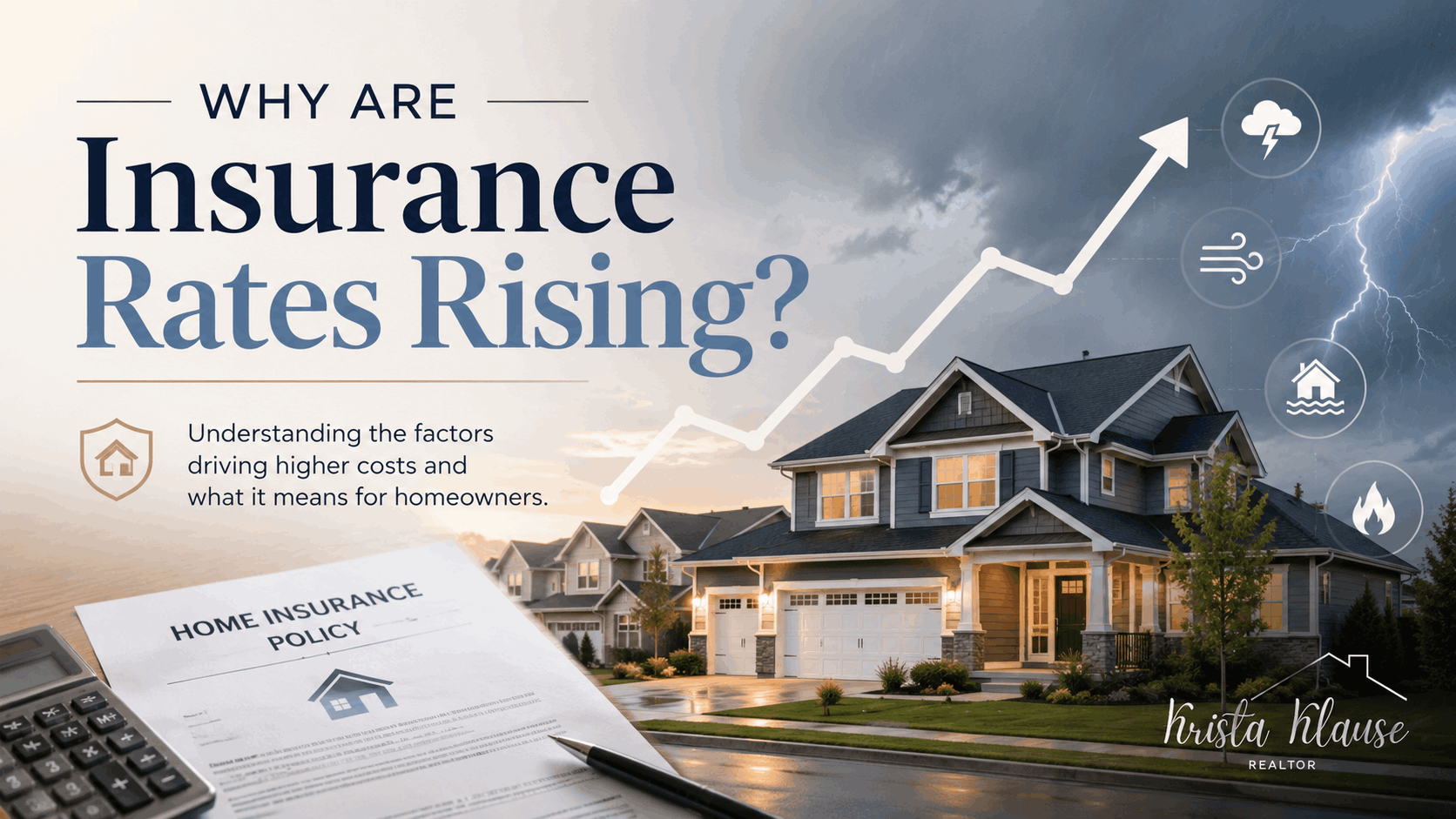

Why Premiums Are Going Up 📊

Insurance rates rise when expected claims become more expensive. A few major factors are pushing premiums higher right now:

-

Rebuilding costs are up because labor and materials cost more than they did a decade ago.

-

Home values have increased, so insurers are covering more expensive assets.

-

Weather-related risks are more frequent in some regions, especially where hurricanes, floods, wildfires, or severe storms are concerns.

That combination means even a small rate increase can add up fast. For example, a home that once cost about $3,000 a year to insure could now be closer to $4,000. That extra amount may not sound huge at first, but over a year it can meaningfully affect affordability.

Why Location Matters So Much 📍

Unlike mortgage rates, which are largely national, insurance is very local. Two homes with similar prices can have very different premiums depending on where they’re located.

If you’re in a higher-risk area, you may pay much more for coverage than someone in a lower-risk market. That’s because insurers price risk based on the chance of future claims, and that risk is not the same everywhere.

For buyers, that means affordability isn’t just about the list price or the mortgage rate anymore. Insurance can change how much house you can truly afford.

How Insurance Affects Monthly Payments 💵

Home affordability is really about the total monthly payment. That includes:

-

Principal and interest.

-

Property taxes.

-

Homeowners insurance.

-

Maintenance and other ownership costs.

As insurance costs rise, they reduce the amount a buyer can put toward the mortgage itself. In other words, higher insurance premiums can lower a buyer’s purchasing power, even if home prices and mortgage rates stay the same.

That’s why insurance is becoming a bigger part of the affordability conversation in 2026.

What Buyers Should Do Next ✅

If you’re planning to buy a home, don’t just focus on the mortgage rate. Make sure you also factor in insurance costs based on the specific home and location you’re considering.

A trusted local agent and lender can help you:

-

Estimate the full monthly payment.

-

Compare insurance costs in different neighborhoods.

-

Avoid surprises before you make an offer.

-

Build a budget that fits your real-life numbers.

That extra planning can make a big difference in what home feels affordable and sustainable for you.

Bottom Line 💬

Homeowners insurance may not get as much attention as mortgage rates, but it plays a major role in what it really costs to own a home. Rising premiums can quietly change affordability, especially in areas with higher rebuilding costs or weather risk.

If you’re thinking about buying or selling in San Antonio, Bandera, Helotes, or surrounding areas, call Krista Klause, your trusted realtor serving San Antonio, Bandera, Helotes, and surrounding areas, to talk through the full cost of homeownership and make a plan that works for your budget. 📲🏡

Categories

Recent Posts